CALIFORNIA INSURANCE Commissioner Ricardo Lara has ordered that the state’s average benchmark workers’ compensation rate be cut by 2.1%, starting Sept. 1. The decision rejected the Workers’ Compensation Insurance Rating Bureau’s recommendation that the benchmark rate be raised by 0.9%, citing a slight uptick in claims costs and claims-adjusting costs.

The benchmark rate, also known as the pure premium rate, is a base rate that insurers can use to price their policies. It includes only the cost of claims and claims-adjusting costs and does not take into account other forms of overhead and profits. Each class code gets its own pure premium rate, and some classes may see increases while others may see further decreases. Additionally, insurers are not required to use the pure premium rate and are free to price their policies as they see fit.

Experience Matters

While this year’s pure premium rate will decline, some employers may see higher rate increases or rate reductions, depending on their class code, claims experience, and X-Mod. The decision is a further reflection of the low pricing environment for workers’ compensation, a rare bright spot in an insurance market that has seen hefty rate increases in other lines, such as commercial property and liability coverage. The average benchmark rate will fall to $1.38 per $100 of payroll, down from the current $1.41.

What’s Affecting Rates

The tiny rate-increase recommendation by the Rating Bureau was based on continuing downward pressure on claims costs since last year. Drivers of the recommendation include:

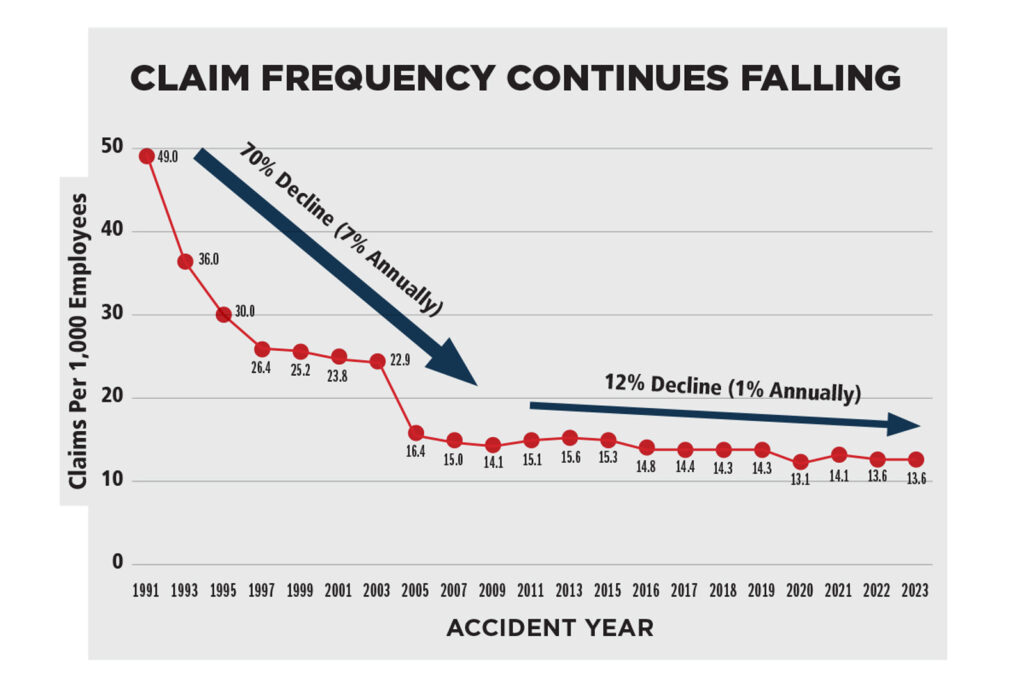

- Lower claims cost inflation

- Lower frequency of claims

- Lower overall claims costs

- Higher medical costs

- Higher claims-adjusting costs

Reasons Behind Lara’s Decision

Factors that the commissioner cited as influencing his decision include:

- The continuing decrease in the number of medical services associated with each workers’ comp claim

- A continuing decline in the percentage of claims with permanent disability benefits

The new rate applies to policies incepting on or after Sept. 1, 2024.